Method, a startup that aims to make it easier for fintech developers to embed repayment, balance transfers and bill pay automation into their apps, today announced that it closed a $16 million Series A funding round led by Andreessen Horowitz, with participation from Y Combinator (Method’s a Y Combinator graduate), Abstract Ventures, SV Angel and others. Co-founder Mit Shah says that the new cash will be put toward product development and growing the company’s headcount from eight people to 28 by the end of the year.

Method launched in 2021 after two of the company’s co-founders, Jose Bethancourt and Marco del Carmen, experienced firsthand the difficulties of embedding debt repayment into their previous company, GradJoy. (TechCrunch previously covered GradJoy, which sought to help students better manage their loan repayment plans through an app-based system.) Integrating student loans into the GradJoy app turned out to be a patchwork of brittle, insecure screen-scraping APIs, physical check mailing and compliance hurdles, according to Shah.

“Jose and Marco realized that there was an opportunity to provide developers with an embeddable API to add debt repayment to their apps and services,” Shah told TechCrunch in an email interview. “In May 2021, we started Method to provide developers with a turnkey infrastructure.”

Shah points out that there’s no standard, technically easy way to access all of a person’s financial liabilities — their student loans, credit cards, mortgages and so on — and push money to those liabilities. Due to the lack of standardization, newer-age fintechs have resorted to using screen scrapers and login credential-based methods to aggregate and access the data, he says. But there’s a downside to those approaches. It can take a long time to onboard new financial institutions, and the lack of a direct connection makes it impossible to perform actions, like paying loans, on users’ behalves.

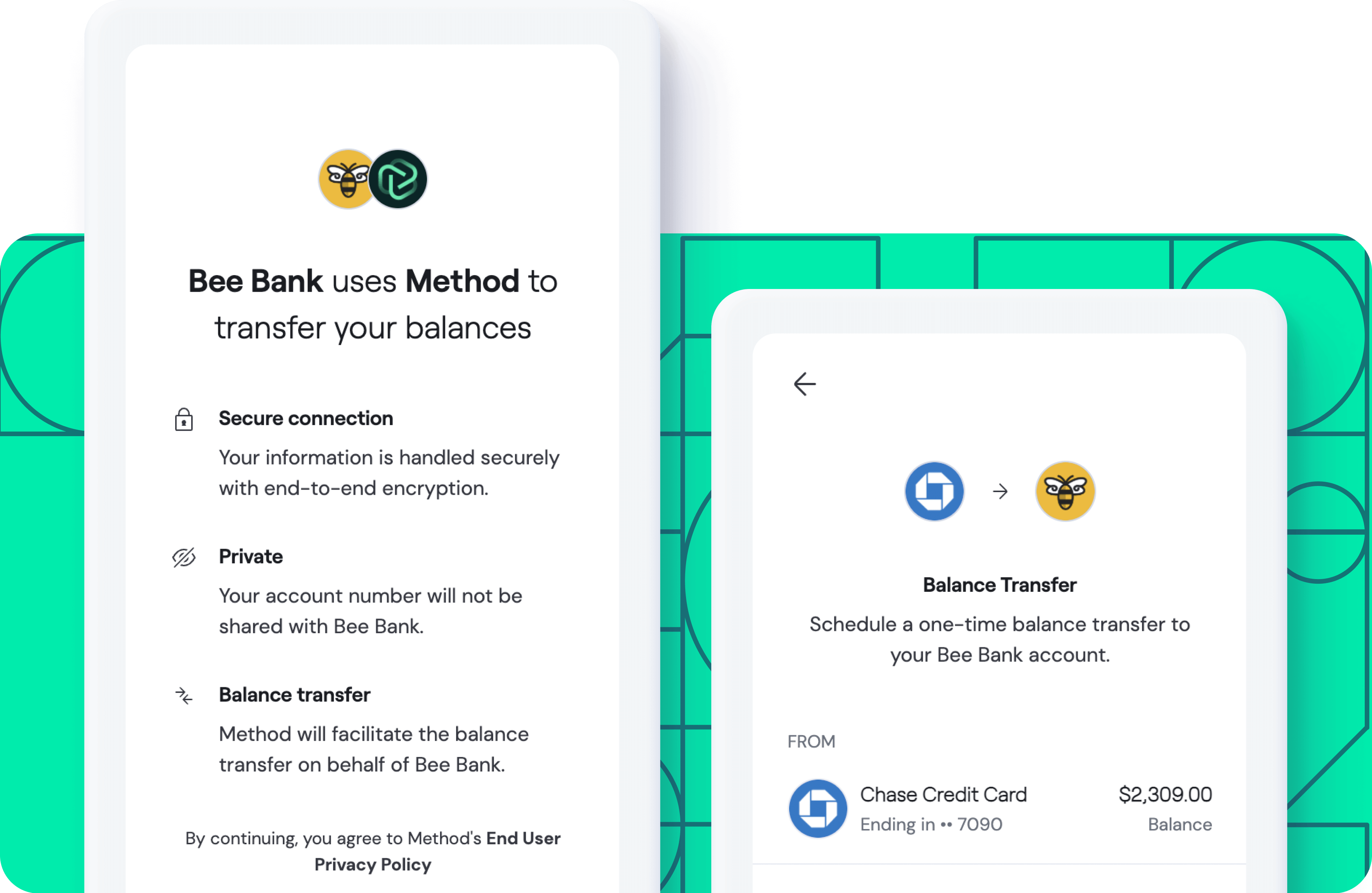

Image Credits: Method

“The industry has been chasing ‘open finance’ by developing solutions around user credentials and working indirectly with financial institutions,” Shah said. “We go straight to the source to enable read and write access for all of a consumer’s liabilities.”

Method works by leveraging consumer credit access protections enacted into law as part of the 2010 Dodd-Frank Act. Tapping into identity verification data from credit bureaus (e.g. Equifax) and wireless carriers (e.g. T-Mobile) and combining it with real-time data from financial institutions’ core banking systems, Method can collate a person’s liabilities across more than 60,000 institutions in the U.S. and kick off tasks such as balance transfers, payoffs, bill pay and more.

“Method’s data API allows our customers — consumer-facing businesses — to retrieve all of a user’s existing liabilities using just their phone number. The liability accounts, once connected, are instantly writable and payable,” Shah explained. “Method’s payment API, meanwhile, allows users to push funds to any type of consumer debt and bill. Method handles the entire money movement process end-to-end, leaving you out of the flow of funds.”

Method handles a lot of sensitive data, which might give some end-customers pause. But Shah said the company’s privacy policy is written to allay consumer advocates’ fears, specifying that Method collects only “minimum user information” and doesn’t sell user data to third parties. In another step to establish trust, the startup’s planning to launch a portal where users will be able to log in with Method to manage the data they share with other apps and services.

Method claims it has 35 customers and more than 75,000 users, with annual recurring revenue sitting at around $2.25 million. While the startup competes with big names like Plaid, MX, Spinwheel and Dwolla, Shah sees Method holding its own, particularly as the platform rolls out new features in the next few months including real-time credit card transactions, instant balance transfers and enhanced live data points for liabilities.

“Currently, new-age fintechs don’t have access to [sophisticated] infrastructure and traditional finance institutions have manual processes set up to retrieve real-time data on consumer credit lines or make payments towards them via checks,” Shah said. “We provide fintechs the ability to innovate faster and compete with larger banks with our turnkey real time data and payment operations. Traditional institutions can onboard users faster and see large savings on manual back end processes … We’ve seen demand for our product from all areas of traditional finance and new-age fintechs in the lending, debt consolidation and personal finance management space.”

To date, Method has raised $18.5 million in venture capital.